Hyperliquid Thesis: The Road to Financial Aggregation

In Q4 2024 Syncracy built a large position in HYPE. In Q1 2025, Syncracy added to its position as the Hyperliquid story accelerated beyond expectations and our conviction grew.

We believe Hyperliquid possesses a unique revenue engine, fusing an exchange and smart contract platform, that positions it to become the highest fee-generating blockchain in the cryptoeconomy. Furthermore, its vertically integrated design, combining these two businesses through a unified interface, enables Hyperliquid to aggregate users more effectively than any peers to date, providing structural advantages in its ambition to house all global finance.

The exchange alone has the potential to disrupt Binance long-term, offering superior performance over decentralized peers, and structural advantages over centralized exchanges in cost, accessibility, auditability, composability, safety, and asset availability. Meanwhile, its smart contract platform has the potential to become one of the leading application ecosystems, leveraging Hyperliquid’s exchange and captive base of traders as the foundation for growth.

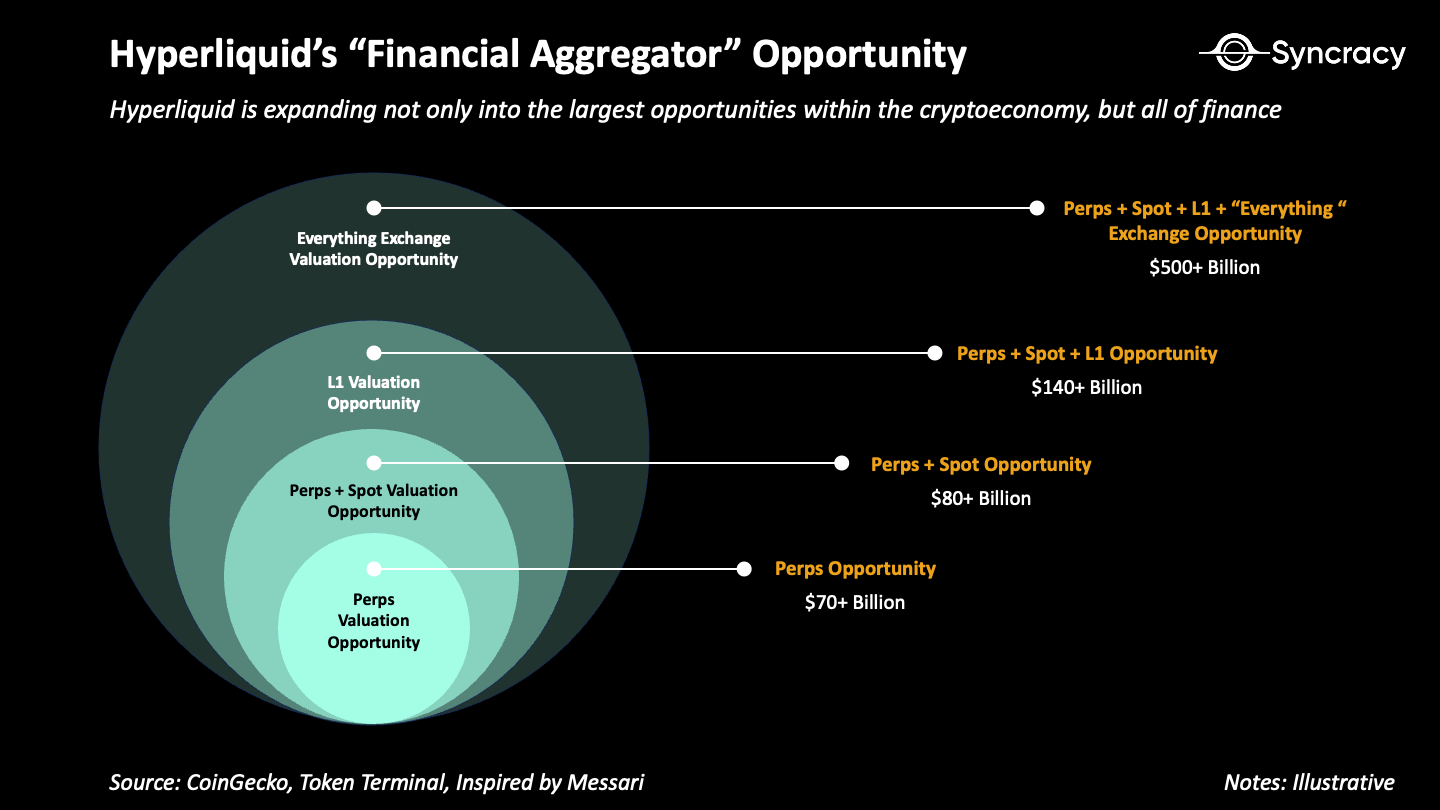

We estimate the combined market size of its exchange and smart contract platform, which we deem the “Financial Aggregator” opportunity, to be valued in the centi-billions of dollars over the coming years.

Below we share our thesis.

Note: Inspired by Frictionless Capital

The Art of Progressive Decentralization

Trading is one of the cryptoeconomy’s clearest killer applications to-date, yet most of it is still done in centralized venues. Is it possible instead to build a decentralized exchange with a Bitcoin-like genesis? This is the question Hyperliquid co-founder, Jeff Yan, set out to answer in 2022 when he launched a new exchange out of the ashes of FTX.

Following a successful quantitative trading career at Hudson River Trading, Jeff found himself in a comfortable position to take a big entrepreneurial leap and launch Hyperliquid with his former Harvard classmate and co-founder Iliensinc. Notably, the team did not take any outside funding from venture capitalists and instead decided to bootstrap the entire project themselves. This was a key decision that allowed the team to both focus on building a product they believe in without external pressure, and eventually distribute the majority of the ownership to the community.

Two years later, Hyperliquid has become one of the fastest-growing projects in the cryptoeconomy, commanding over 60% market share in the onchain perps market. In doing so, it has played a pivotal role in spearheading the shift to onchain perps trading, which now accounts for 12% of global trading volumes.

What’s been Hyperliquid’s key to success?

It all starts with the team's product-first philosophy. Rather than optimizing for ideological purity, such as prioritizing maximal decentralization from day one, the team instead optimized for delivering the best possible onchain trading experience. This strategy is best understood as progressive decentralization – a practical approach for building a winning project in the cryptoeconomy, that involves teams first finding product-market fit, then gradually relinquishing control over time.

The key insight that the team understood is that while decentralization and open-source software are crucial in the long-run in order to reduce counterparty risk and enable greater product scalability, most users preferred performance and usability over rigid adherence to cypherpunk principles. So for the two years leading up to the HYPE token launch, the team relentlessly refined the platform through direct engagement with traders.

This feedback loop proved invaluable as the Hyperliquid team frequently implemented feature requests and bug fixes within hours, building deep trust within the community. It also led to key product features such as order cancel prioritization for traders, which enables market makers to quote tighter spreads, and Hyperliquid vaults, which enables the exchange to quickly bootstrap liquidity for new pairs. The result was a high-performance chain with an enshrined orderbook (CLOB) capable of 100K transactions-per-second (tps) throughput and sub-second finality – an order of magnitude performance improvement over peers.

As volumes grew exponentially into year-end 2024, the Hyperliquid team executed its most ambitious move yet – airdropping 31% of its token supply to its users. The airdrop was an overwhelming success because Hyperliquid already had proven product-market-fit – a stark contrast to most other projects that list their tokens publicly prematurely.

Crucially, the HYPE token also had clear intrinsic value, with fees run-rating at $228M per year at the time. This not only provided strong incentives for recipients to hold rather than immediately sell, but also created strong buying pressure for HYPE as the fees fueled large scale buybacks. Additionally, with no pre-allocations to any insiders beyond the core team, the airdrop created a scenario where any large buyers who wanted exposure were required to buy in public markets. This was a strategic masterstroke as it not only forced these players to onboard directly onto Hyperliquid, increasing volumes in lockstep, but also highlighted Hyperliquid’s next evolution as more than a simple derivatives exchange, first starting with spot markets.

The Everything Exchange

Exchanges are winner-take-most markets, where liquidity network effects, scale efficiencies, brand equity, and regulatory moats concentrate trading activity among a few dominant players. This pattern has shaped financial markets for centuries, cementing the dominance of leaders such as CME in derivatives, NYSE and Nasdaq in equities, and Binance in centralized crypto markets. Yet, despite their scale, no exchange has ever fully unified liquidity across multiple asset classes on a single global ledger – a concept we call the “Everything” Exchange.

Bridging this gap requires more than just dominance in a single market – it demands infrastructure that can seamlessly integrate multiple asset classes, unify liquidity, and scale globally. This is where Hyperliquid’s design diverges from traditional exchanges, offering a vertically integrated system that consolidates liquidity across both spot and derivatives markets while operating on its own high-performance blockchain.

Blockchain based exchanges provide structural advantages in auditability, efficiency, safety, composability, and accessibility. Instead of entrusting assets to centralized entities with opaque risk, users can self-custody assets and trade in global, 24/7, near-instantly settled markets using autonomous smart contracts as intermediaries.

These benefits aren’t just theoretical. They’re already driving volumes onchain today. This trend is not only observable in the data, but also in the strategy of two of the largest exchanges in the industry, Binance and Coinbase, which launched their own respective blockchains – Binance Smart Chain (BSC) and Base – to position ahead of this transition.

Hyperliquid understands this opportunity and is already taking its first step towards it through expanding into crypto spot markets. The solution starts with enabling users to send native assets from blockchains such as Bitcoin, Ethereum, and Solana to Hyperliquid through an enshrined interface. This is a first for an onchain exchange as historically all have either been single-chain or spot only. Hyperliquid will be the only onchain CLOB to feature both multi-chain spot and derivatives markets, replicating the centralized exchange experience onchain for the first time in history.

With HYPE and BTC as the only large cap asset that Hyperliquid currently supports in its spot markets, it is already a top 10 DEX and top 5 chain by DEX volumes in the world. We anticipate it will rapidly climb up the ranks as it imports the largest assets in the cryptoeconomy to trade, adding 9 figures of earnings within the first year post launch, assuming spot volumes reach 30% of Perps volumes, as is the typical ratio for exchanges that service both markets.

Hyperliquid should continue to outcompete its centralized peers due to its advantages in:

Cost – significantly lower trading fees and overhead than CEXs like Binance

Accessibility – easier for users to onboard due to its global permissionless nature

Auditability – easy to verify using basic public-key cryptography inherent in blockchains

Composability – easy for third parties to develop atop of (e.g builder codes)

Safety – self-custodial with chain decentralization improving over time

Asset availability – quicker, more transparent process for asset listings

Moreover, these advantages enable Hyperliquid to eventually expand beyond blockchain-native assets. As tokenization efforts accelerate Hyperliquid’s opportunity may encompass all assets globally including currencies, stocks, bonds, commodities, real estate, and even exotic markets such as sports betting and prediction markets. In fact, we believe this shift is practically inevitable. As wallet adoption grows, asset issuers will have an increasingly strong incentive to list on public blockchains to tap into a global investor base for increased distribution and for access to the lowest cost of capital.

Zooming out, we estimate the opportunity within the cryptoeconomy today is worth over $140B+. We furthermore estimate the opportunity beyond the cryptoeconomy, which encompasses every asset class and exchange on the planet, to be worth a minimum of $500B+ globally, which doesn’t include private exchanges, exotic assets, or large OTC markets like foreign exchange. Inclusive of those, the market opportunity would easily enter the trillions of dollars. Again, we believe that blockchain based exchanges are a massive expansion of the exchange opportunity.

Note: you can find our valuation assumptions in our model here

In its short history, Hyperliquid has already achieved a $577M annual run-rate in revenue solely from its perps exchange and adolescent spot markets. Should any of the above thesis play out over the coming 12 - 24 months, we expect revenue to expand multiples going forward, likely catapulting Hyperliquid to the top of the cryptoeconomy in terms of onchain revenue (it is already #3).

The Road to Financial Aggregation

The “everything exchange” opportunity alone provides more than enough potential to get excited about with its multi-trillion dollar TAM. Could there possibly be even more to the story?

In the prior section we mentioned how Binance and Coinbase launched BSC and Base, respectively. The two chains are separate entities from the exchanges, with separate cap tables and PnLs. But what if, for example, Binance and BSC were combined? What if in essence you combined two of the most profitable businesses in the history of the cryptoeconomy: exchanges and smart contract platforms? What if you furthermore made them both accessible through a single interface? This is the opportunity Hyperliquid has with its recently launched HyperEVM, an EVM compatible virtual machine that will run in parallel with its order book exchange.

We believe that with its exchange as the initial killer app that directly owns user order flow, Hyperliquid is well positioned to become one of the cryptoeconomy’s first aggregators. In essence, by tightly integrating its interface, exchange, and smart contract platform into one cohesive experience, Hyperliquid can aggregate users at scale, creating unmatched leverage over developers and asset issuers compared to peers.

This is a big deal as historically the three have been fragmented in the cryptoeconomy. For example, Base is Ethereum’s most successful rollup, but is mostly separate from the broader Coinbase product suite and primarily accessed through third party interfaces. Uniswap verticalized the wallet, interface, order router, exchange, and rollup, but inherited Ethereum’s technical debt from its messy modular roadmap. Solana is the most used blockchain in the cryptoeconomy, yet outsources the user experience to external builders like Pump and Jupiter, the latter of which is partially leaving to launch its own chain.

In contrast, Hyperliquid integrates the entire stack, only partially modularizing its application and interface layers – a design choice that creates a potential strategic advantage. Unlike ecosystems that rely entirely on third-party applications and interfaces, Hyperliquid’s in-house exchange serves as both an anchor and a distribution hub, reinforcing its network effects. The exchange serves as a top-of-funnel for third-party developers to build applications and issue assets that can integrate directly with the flagship Hyperliquid interface, where users are concentrated. This creates a powerful feedback loop. The more users on the exchange, the more liquidity is available to applications. The more liquidity available to applications, the more useful the applications become. The more useful the applications become, the stickier the Hyperliquid ecosystem, and the more valuable Hyperliquid becomes over time.

Pulling this all together, the shared state between the Hyperliquid exchange and the HyperEVM could lead to a number of synergies and product innovations such as:

Advanced Collateral Management – a prime brokerage app that makes it simple for traders to achieve maximum capital efficiency on their collateral – e.g. lending out liquid staked HYPE via an Aave-like protocol, selling the interest through a yield market like Pendle, while simultaneously using that position as collateral for a derivatives trade

Onchain Structured Products – an asset management app that leverages Hyperliquid vaults and derivatives to create onchain structured products similar to Ethena

Social Trading – a social trading app can expand its group trading strategies through Hyperliquid vaults or allow traders to automatically capture a portion of copy trading fees through builder codes

Advanced Money Markets – a money market protocol that integrates Hyperliquid’s derivatives exchange to hedge collateral risk and spot exchange for liquidations, ultimately enabling it to offer higher loan-to-value (LTV) ratios for borrowers

Private Trading – a privacy protocol akin to Tornado Cash that enables anonymous order placement (Dark Pools) on Hyperliquid’s exchange

These examples barely scratch the surface – the deep integration between Hyperliquid’s trading interface, order book, and smart contract ecosystem is fertile ground for an entirely new wave of onchain financial primitives.

Hyperliquid has a couple of important levers to pull to bootstrap its ecosystem – a key competitive advantage in what is an increasingly saturated smart contract platform landscape. These levers revolve around its captive community of user-owners and its warchest of incentives.

Captive Trading Audience – Unlike most emerging smart contract platforms, Hyperliquid already has a massive, highly engaged user base. This solves the cold-start problem that plagues ecosystems outside of Ethereum, Solana, and Base, giving developers an instant market for their products

Incentive Warchest – at genesis, Hyperliquid allocated 39% of its supply (~$9 billion today) for community rewards and incentives, allowing it to launch a multi-year, multi-billion-dollar campaign to attract users and builders

Assistance Fund Buybacks – Hyperliquid announced it would begin buying ecosystem tokens with its assistance fund to spark onchain activity and support its community

Builders in the HyperEVM ecosystem are acutely aware of these advantages and are structuring their go-to-market strategies accordingly. Many are inspired by Jeff and extremely aligned with HYPE holders, which will likely lead to many airdropping their token supplies to Hyperliquid users and HYPE stakers. This dynamic can be understood similarly to Binance’s launchpad – one of the biggest demand drivers for BNB (next to its exchange revenues), which even today commands a $90 billion valuation despite BSC being practically dead.

Additionally, there’s a handful of projects promising to allocate a portion of their treasury to HYPE, which may create additional demand for HYPE as they ramp up revenue. This may be important in developing the story of HYPE as a non-sovereign store of value similar to ETH and SOL which are also the reserve assets of their ecosystems. As HYPE adoption scales across the HyperEVM, its role as gas, collateral, and a quote pair will further this narrative, potentially enabling HYPE to command valuations far beyond what MEV and execution fees alone would justify. This would cement its status as a core asset in the cryptoeconomy alongside BTC, ETH, and SOL.

Hyperfinancialization

As time passes, breaking into the exchange or smart contract platform markets is becoming an increasingly formidable challenge. Both are network-effect-driven businesses, dominated by entrenched global leaders, and likely to consolidate into power-law market structures over time. Competing in these arenas without a distinct and compelling value proposition is not just difficult – it’s foolish.

We believe Hyperliquid is one of those rare new entrants that can meaningfully dent both markets. Its vertically integrated design, coupled with a product-first mentality, has made it one of the fastest-growing projects in the history of the cryptoeconomy. More importantly, Hyperliquid has a unique revenue engine and is positioned to become the highest fee-generating blockchain in the world by capturing both exchange and smart contract platform fees – an advantage no other smart contract platform or exchange can claim.

Of course, the thesis is not without risk. Beyond the execution risks inherent in any early stage venture, there are risks related to:

Centralization – Hyperliquid may not be able to globally distribute its validator set, which currently consists of 16 co-located servers in Tokyo, without performance degradation; moreover its inability to decentralize may open regulatory risk

Developer Ecosystem Buildout – Hyperliquid has primarily been developed by the core team with minimal outside contribution; with much of the code still closed source and the HyperEVM in its infancy it could be an extended buildout towards a robust ecosystem of third party contributors

Protocol Enshrinement – It's an open question whether it makes sense to enshrine all of the infrastructure necessary to run an order book exchange onchain, especially as it relates to the perpetual swaps product which requires a protocol-owned insurance fund to protect against insolvencies – an exposure Ethereum and Solana do not carry, as they outsource solvency risk to third-party exchanges built on their platforms

Bridge Hacks – Hyperliquid’s spot markets may be undermined if it cannot convincingly decentralize its bridging infrastructure; moreover lack of native stablecoin support creates unnecessary counterparty risk

Business Cyclicality – Exchanges are cyclical businesses and declining interest in the asset class will lead to lower volumes and lower fees

Despite these risks, Hyperliquid’s track record speaks for itself. Time and again, the team has demonstrated world-class execution, with no signs of slowing down. Perhaps that is the most important factor of all, given how early Hyperliquid is in its life cycle.

It is rare to find founders operating at this level. Even rarer to find them building simultaneously in two of crypto’s largest markets. Our experience has taught us that when you encounter opportunities of this magnitude, it pays to bet, and bet in size.

The cryptoeconomy is evolving from the old guard of ideologically-motivated dreamers to commercially-oriented builders who will deliver blockchains to the masses.

The lines between financial markets are dissolving, converging into a single, composable, hyperliquid financial system. In time, the old financial world’s collection of siloed ledgers, intermediaries, and clearinghouses will give way to one unified, real-time, programmable economy.

We’re excited to back Hyperliquid as it makes a run towards this vision.

The road to Hyperfinancialization is in full swing.

Hyperliquid.

Special thanks to Shoku, Sean Lippel, Felipe Montealegre, Kel Eleje, and Sunny Shi for their feedback and review.

Important Legal Notices

While this article is intended to express the views held by Syncracy Fund Management LLC (“Syncracy”), nothing in this article is intended to constitute or form part of, and should not be construed as, an issue for sale or subscription of, or solicitation of any offer or invitation to subscribe for, underwrite, or otherwise acquire or dispose of any security, including any interest in any private investment fund managed by Syncracy. Any such offer may only be made pursuant to a formal confidential private placement memorandum of any such fund, which may be furnished to potential investors upon request and which will contain important information to be considered in connection with any such investment, including risk factors associated with making any investment in any such fund. Further, nothing in this correspondence is, or is intended to be treated as, investment or tax advice. Each recipient should consult their own legal, tax and other professional advisors in connection with investment decisions. Any investment involves the risk of a loss, including the risk of a complete loss.

Syncracy’s views with respect to any investment, including HYPE, could change at any time. Further, while Syncracy currently holds a long position in HYPE, Syncracy will not provide any recipient of this article with notice if Syncracy unwinds its position or its views change.